In-depth analysis of Skyworks

We analyze this top position in the WideAlpha AI-Selected Index

Of the top positions in the WideAlpha AI-Selected Index one that we find particularly intriguing is Skyworks (SWKS). Given that the AI that manages this index uses deep neural networks, it is not possible to know exactly the reasons it chooses one company over the other except that it estimates the company has a high probability of outperforming the market over the next 3-5 years. However, by looking at the financials we can get an idea, and many of the inputs to the system include growth and valuation measures.

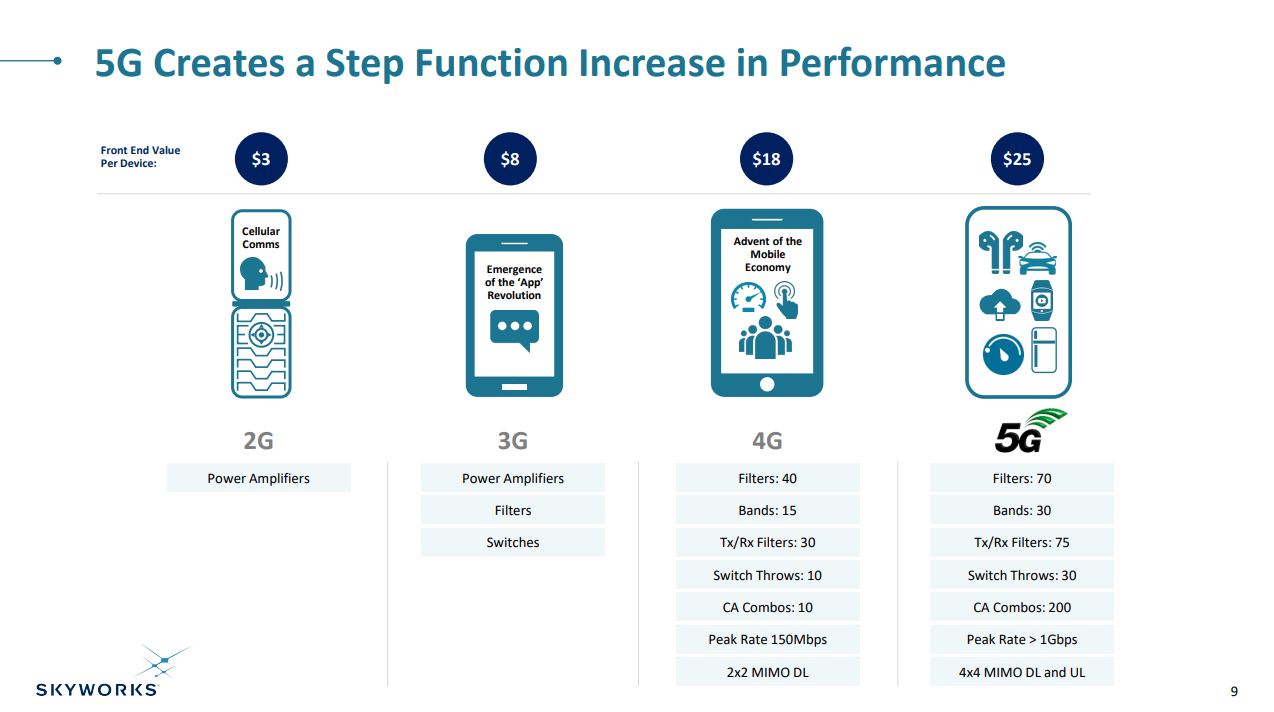

Skyworks is getting a growth boost from the transition to 5G. As can be seen in the image below it gets a lot more revenue from a 5G device compared to a 4G device. This should accelerate revenue growth and profitability.

Source: Skyworks Investor Relations

Despite this growth tailwind shares are not particularly expensive, trading at a trailing twelve months P/E ratio of ~15x, and a forward P/E of ~12x. This does not strike us as particularly expensive for a quality company that is expected to grow revenue and profits for the next few years, and which has a strong IP portfolio.

Admittedly, growth seems to come in bursts and there have been periods where growth was negative, but in general the company has been growing, some quarters at a more than 50% rate.

Despite the existence of some cyclicallity in its results, looking directly at revenue and net income for the last few years it is clear that the trend is up.

Turning our attention to the balance sheet, it is quite solid with relatively low leverage. It used to have a net cash balance, but some recent bolt-on acquisitions such as the acquisition of the infrastructure and automotive business from Silicon Labs, as well as spending on share repurchases have drained the cash coffers. Still, the company maintains a strong balance sheet with financial debt to EBITDA of < 1x.

We’ll finish just pointing out the quality of the business, not many companies have free cash flow margins > 30%, operating margins of ~40%, and gross margins >50%, and are growing faster than their market. Skyworks is the rare company that has terrific financials, strong competitive advantages, and yet trades at a reasonable valuation.

Source: Skyworks Investor Relations

Conclusion

We agree with AlphaPilot that Skyworks should be a top position in the index, we like what we see here, and think this is a great company at a very reasonable valuation. It has some risks, such as an over-dependence on Apple as a customer (Apple is by far the biggest customer of Skywork’s RF devices). Still, the company appears to be experiencing accelerating growth from the transition to 5G, and growth from IoT applications. We look forward to following Skywork’s progress and its contribution to the WideAlpha AI-Selected Index returns.

Disclaimer: All material presented in this newsletter is not to be regarded as investment advice, but for general informational purposes only. We cannot guarantee profits or freedom from loss. You assume the entire cost and risk of any trading you choose to undertake. You are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, its moderators, and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer.